Coinbase Wallet Taxes

Coinbase Wallet Taxes provides a comprehensive guide to understanding how your Coinbase wallet is taxed. The article covers topics such as what types of taxes you may owe on your Coinbase wallet, how to calculate your taxes, and how to file your taxes.

Coinbase Wallet Taxes: How to Avoid Them

The IRS has a list of common tax issues Coinbase Wallet users may face. One such issue is paying taxes on cryptocurrency transactions. Here are some tips to help avoid taxes on your Coinbase Wallet transactions:

1. Use a tax preparer.

If you're not able to figure out how to pay taxes on your own, it's recommended that you use a tax preparer. A tax preparer can help you navigate the complex tax laws surrounding cryptocurrency transactions, and they can also help you file your taxes in a timely manner.

2. Make sure you're filing the correct forms.

If you're using Coinbase Wallet to purchase cryptocurrency, you'll need to file Form 8949 with your tax return. This form is used to report income from cryptocurrency transactions.

3. Pay your taxes early.

If you can afford to do so, it's always best to pay your taxes early. This will give you more time to figure out any mistakes that may have been made, and it will also reduce the amount of money that you'll have to pay in taxes.

4. Use a cryptocurrency IRA.

If you're interested in using cryptocurrencies for investment purposes, you may be eligible to invest in a cryptocurrency IRA. This type of account allows you to invest in cryptocurrency without having to worry about taxes.

5. Sell your cryptocurrencies and pay taxes on the proceeds.

If you want to sell your cryptocurrencies and pay taxes on the proceeds, you'll need to follow tax guidelines specific to cryptocurrency transactions. You can find more information about this process on the IRS website.

Coinbase Wallet Taxes: What You Need to Know

If you are an individual living in the United States, you are subject to federal income taxes on all your income. Coinbase Wallet taxes will apply to any taxable income that is generated from your Coinbase Wallet activities.

The most important thing to know about Coinbase Wallet taxes is that you are responsible for reporting all of your income from your Coinbase Wallet activities. This means that you will need to report all of the money that you earn from trading cryptocurrencies and other digital assets, as well as any money that you earn from fees that you charge to customers.

You will also need to report any taxable income that is generated from your Coinbase Wallet activities when you file your federal income taxes. This means that you will need to include all of your trading income, as well as any money that you earn from fees that you charge to customers.

It is important to keep track of your Coinbase Wallet taxes so that you can accurately report all of your income. If you have any questions about Coinbase Wallet taxes, please contact your tax professional.

Coinbase Wallet Taxes: Tips to Save You Money

If you are a Coinbase wallet user in the United States, you may be subject to taxes on your gains. Here are some tips to help you save money on taxes:

1. Review your tax bracket and see if you are in a higher or lower tax bracket.

2. Review your income and see if you have any special deductions that could reduce your tax bill.

3. Consider using tax software to help you calculate your taxes.

4. Save your receipts from your Coinbase transactions so you can track your tax savings.

Coinbase Wallet Taxes: How to Save on Them

When it comes to taxes, there are a few things you can do to save on Coinbase Wallet.

First, make sure to review your Coinbase account and transactions for accuracy. This will help you keep track of any potential tax deductions and credits you may be eligible for.

Next, open a Coinbase account if you don’t already have one. This will allow you to make tax-deductible purchases and transfers from your bank account.

Finally, consult with a tax professional if you have any questions about how to save on Coinbase Wallet taxes. They can help you understand your specific situation and recommend the best way to reduce your tax liability.

Coinbase Wallet Taxes: The Basics

Coinbase Wallet Taxes: The Basics

When you use Coinbase to buy and sell cryptocurrencies, you may be subject to federal and state taxes. Here’s a look at the basics of how taxes work with Coinbase and cryptocurrencies.

What are taxes?

Taxes are payments made by individuals, businesses, and governments to fund various government programs. In the U.S., taxes are paid by individuals on their income, businesses on their profits, and governments on the value of goods and services sold.

How do taxes work with Coinbase and cryptocurrencies?

When you use Coinbase to buy and sell cryptocurrencies, you’re likely paying taxes on those transactions. Coinbase takes a fee from each transaction, and then pays taxes on that fee. So, in effect, you’re both paying taxes and getting paid by Coinbase.

Which taxes are applicable to Coinbase and cryptocurrencies?

In general, taxes are applicable to any transactions that take place using cryptocurrencies. However, there are a few exceptions. For example, transactions involving goods and services that are used in your regular business operations are exempt from most taxes. So, if you use Coinbase to buy goods or services for your own use, those transactions aren’t taxable.

Additionally, many cryptocurrencies are not considered “money” under federal law. This means that most cryptocurrencies don’t fall under the purview of federal income taxes, capital gains taxes, or other tax obligations. Instead, these taxes apply only to traditional money (like U.S. dollars and Euros). So, if you make a purchase using Ethereum or another cryptocurrency, you likely won’t have to pay any federal taxes on that transaction.

However, there are some exceptions to this rule. For example, if you sell goods or services using a cryptocurrency that was obtained as a result of mining or trading cryptocurrencies, you may have to pay capital gains taxes on that sale.

For more information on cryptocurrency taxes, see our guide on cryptocurrency taxation.

Can I avoid paying taxes on my Coinbase transactions?

There’s no guarantee that you’ll avoid paying taxes on your Coinbase transactions. However, there are a few things you can do to reduce your tax burden.

First, consult with an accountant or tax preparer to see if you have any special tax obligations related to your Coinbase transactions.

Second, try to make your Coinbase transactions using cryptocurrencies that are not subject to federal or state taxes. This will reduce your tax liability overall.

Finally, consider using a tax-advantaged account like a Roth IRA or 401k to help offset some of your tax liability. These accounts allow you to pay taxes on your cryptocurrency earnings at a later time, rather than immediately paying those taxes when you receive them in your regular checking or savings account.

For more information on avoiding cryptocurrency taxes, see our guide on cryptocurrency taxation.

Coinbase Wallet Taxes: What You Should Know

Coinbase Wallet Taxes: What You Should Know

If you're an American taxpayer, you should be aware of the taxes that Coinbase will charge you when you use their wallet. Coinbase charges a 0.25% transaction fee on all transactions, and they also charge a 1.49% sales tax in most states. This means that if you make a purchase with your Coinbase wallet, you'll end up paying $0.04 in taxes.

Coinbase Wallet Taxes: A Beginner's Guide

Once you have created a Coinbase wallet, you are ready to start trading and investing in digital assets. One important thing to keep in mind is that you will likely have to pay taxes on any profits you make from trading and investing in digital assets. In this guide, we will discuss the tax implications of trading and investing in digital assets on Coinbase.

What Are Bitcoin and Ethereum?

Bitcoin and Ethereum are two of the most popular cryptocurrencies on the market. Bitcoin is a digital asset that was created in 2009 and is based on the blockchain technology. Ethereum is a more recent cryptocurrency that was created in 2015 and is also based on the blockchain technology.

How Are Bitcoin and Ethereum Taxed?

Bitcoin and Ethereum are treated as capital assets for tax purposes. This means that you will pay capital gains taxes when you sell them and you will also pay income taxes on the profits you make from trading and investing in them.

How Are Bitcoin and Ethereum Taxed When You Mine Them?

Bitcoin and Ethereum are mined using specialized computer hardware. When you mine them, you are actually earning rewards in cryptocurrency. These rewards are typically sent to your wallet automatically. However, if you sell the cryptocurrency that you mined, you may have to pay capital gains taxes on the value of the cryptocurrency. And if you sell the cryptocurrency while it is still worth a lot of money, you may have to pay income taxes on the profits you make.

How Are Bitcoin and Ethereum Taxed When You Earn Them?

When you earn Bitcoin or Ethereum, you are generally just receiving a payment in cryptocurrency. This means that you will not have to pay taxes on the value of the cryptocurrency when you receive it. However, if you sell the cryptocurrency, you may have to pay capital gains taxes on the value of the cryptocurrency and/or income taxes on the profits you make from selling it.

Can I Use Bitcoin or Ethereum To Pay My Bills?

Yes, you can use Bitcoin or Ethereum to pay your bills. However, note that this may not be a good long-term strategy for saving money. If the value of Bitcoin or Ethereum decreases over time, you may end up losing a lot of money. Instead, it may be a better strategy to use these currencies to purchase goods and services.

Coinbase Wallet Taxes: An Overview

If you are a Coinbase user, you may be wondering about the taxation of your transactions. In this article, we will discuss the types of taxes that may apply to your Coinbase transactions, and how you can avoid them.

Coinbase Wallet Taxes: General Information

There are a few key things to keep in mind when it comes to Coinbase wallet taxes. First and foremost, as a Coinbase user, you are responsible for any and all applicable taxes that may apply to your transactions. Coinbase cannot and does not determine or advise you on which taxes may apply to your transactions.

Second, Coinbase generally charges a 1.49% fee on all transactions, which includes both buy and sell transactions. This fee is automatically included in the prices that you see when you make a purchase or sell on Coinbase.

Finally, it is important to note that there are some specific tax laws that may apply to your Coinbase transactions. For example, if you are selling bitcoins, you may be subject to capital gains tax if you sell them for more than you paid for them. Additionally, if you are buying bitcoins and using them to purchase another cryptocurrency or assets, you may be subject to capital gains tax as well.

Coinbase Wallet Taxes: Buy vs. Sell

When you are selling bitcoins on Coinbase, you are generally selling them for more than you paid for them. This means that you will likely be subject to capital gains tax if you sell them for more than you paid for them.

When you are buying bitcoins on Coinbase, however, you are generally buying them for less than they are worth on the open market. This means that you will likely not be subject to capital gains tax when you purchase bitcoins on Coinbase. However, if you later sell them for more than you paid for them, you may be subject to capital gains tax.

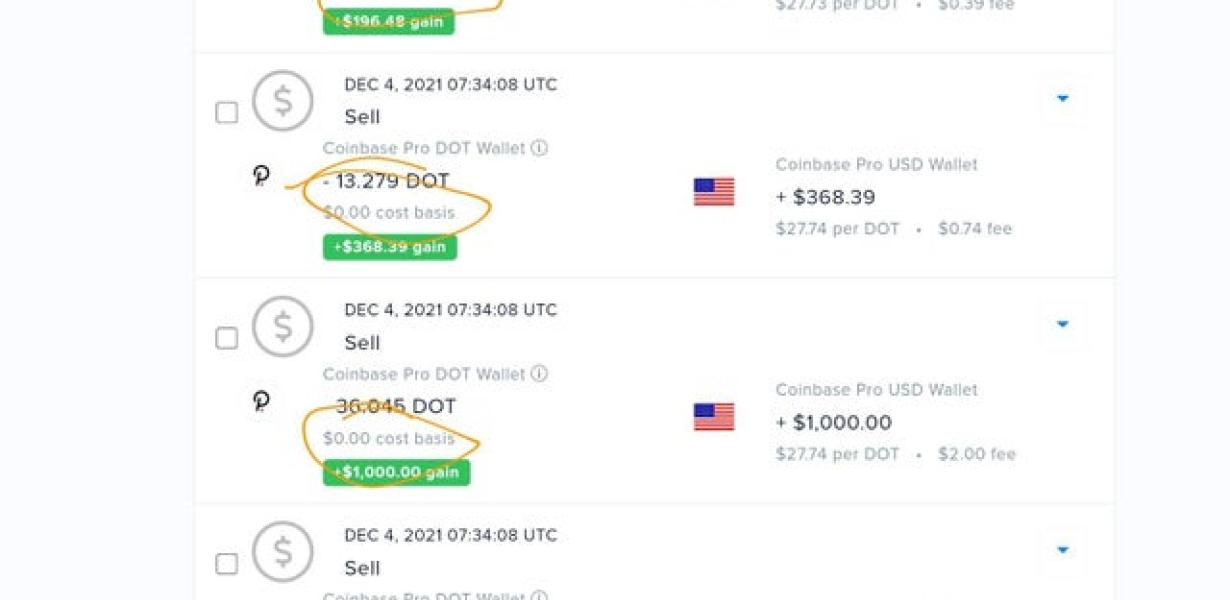

Coinbase Wallet Taxes: Capital Gains Tax

When you sell bitcoins on Coinbase, you may be subject to capital gains tax if you sell them for more than you paid for them. This means that you may be able to claim a tax deduction for the difference between the price at which you sold the bitcoins and the price at which you bought them.

When you purchase bitcoins on Coinbase, however, you are generally not subject to capital gains tax. This means that you will not be able to claim a tax deduction for the difference between the price at which you bought the bitcoins and the price at which you sold them.

Coinbase Wallet Taxes: Crypto Transactions

If you are buying or selling cryptocurrencies on Coinbase, you may be subject to capital gains tax as well. This means that you may be able to claim a tax deduction for the difference between the price at which you bought the cryptocurrencies and the price at which you sold them.

Coinbase Wallet Taxes: Other Tax Laws

There are also other tax laws that may apply to your Coinbase transactions. For example, if you are selling bitcoins for fiat currency (dollars, euros, etc.), you may be subject to income tax as well. Additionally, if you are using bitcoins to purchase assets or cryptocurrencies other than bitcoins, you may be subject to capital gains tax as well.

Coinbase Wallet Taxes: FAQs

What are Coinbase wallet taxes?

When you use a Coinbase wallet to buy or sell cryptocurrencies, you may be subject to capital gains or losses. These taxes can add up, so it's important to know what to expect. Here are some Frequently Asked Questions about Coinbase wallet taxes.

What is a capital gain?

A capital gain is the increase in the value of an asset over a period of time. When you purchase a cryptocurrency using your Coinbase wallet, you may experience a capital gain. This is because the price of the cryptocurrency has increased since you purchased it.

What is a capital loss?

A capital loss is the decrease in the value of an asset over a period of time. When you sell a cryptocurrency using your Coinbase wallet, you may experience a capital loss. This is because the price of the cryptocurrency has decreased since you sold it.

How do I know if I have a capital gain or loss?

If you have made a purchase or sale of cryptocurrencies using your Coinbase wallet in the last 12 months, you will need to report your capital gains or losses on your tax return. You can do this by entering your transactions in the appropriate section of your tax return.

Can I avoid paying taxes on my Coinbase wallet transactions?

Unfortunately, no. You will need to report your capital gains and losses on your tax return, even if you don't pay any taxes on your transactions.

Coinbase Wallet Taxes: Resources

There is no definitive answer to this question as the taxation of digital currencies like Bitcoin is still in its early stages. However, some resources that may be useful include:

-The Bitcoin Foundation: This organization provides information on Bitcoin and digital currency taxation.

-Coinbase: This company provides a Bitcoin wallet and services for buying and selling Bitcoin.

-Blockchain: This website provides information on digital currency wallets, exchanges and other blockchain-related services.